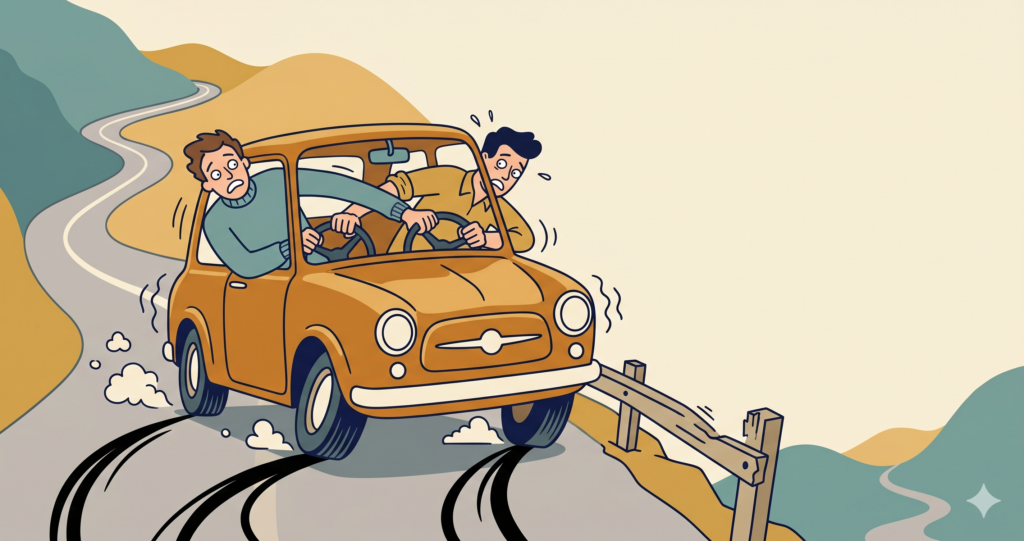

Who’s Driving Your Portfolio?

React to every dip, and you quietly become the second driver — heading for a crash.

Every few weeks, I get a message that goes something like this.

An investor writes in — sometimes early in the morning, sometimes late at night — and the words are almost always the same:

I want to be very honest with you about what the portfolio usually looks like on the day a message like this lands.

It is up. Not a little — very often 20% or more. In plain rupees, the family is frequently sitting on lakhs of profit. Not a single scheme has collapsed. And quite often, the funds they’re most worried about are barely a month or two old — bought just a few weeks ago.

So the real picture is this: solid gains on the screen, nothing broken anywhere — and a genuinely worried investor, convinced that everything is going wrong.

I’m not sharing this to mock anyone. I’ve deliberately blurred every detail, because it isn’t one person — it’s a pattern I’ve watched repeat a hundred times in twenty years. Good, intelligent, hard-working people, all making the same single mistake.

What is your Why?

Why did you start investing in the first place?

Sit with that for a second. Not “which fund.” Not “how much return.” Why.

I already know the answer, because it’s almost always one of these:

- “For my child’s education” — which is 10 years away.

- “For my daughter’s marriage” — 12 years away.

- “For my retirement” — 18, 20 years away.

- “For my own freedom” — so that one day, work becomes a choice, not a compulsion.

Look at those answers again. Every single one of them lives years into the future. Five years. Ten. Fifteen. Twenty.

Now here is the question I want you to ask yourself:

You are measuring a 15-year journey with a 15-day ruler. And then feeling anxious about what the ruler shows. Of course it feels wrong — you’re using the wrong instrument.

Let me show you a real journey

I’m going to show you one fund’s actual history. I am not recommending this fund — please don’t rush to buy it. I’m using it only as an example, because its numbers are real and they tell the truth better than any speech I could give.

Imagine someone who started a simple SIP of ₹10,000 a month in this fund — back in December 1993. And then did the most boring thing imaginable: nothing. They just kept the SIP running. Through every crash. Through every flat year. Through every “this isn’t working” feeling.

Over the years they invested about ₹39 lakh in total — ten thousand at a time. Today that money is worth over ₹22 crore.

Twenty-two crore from thirty-nine lakh. That works out to about 19.5% a year for over thirty years.

Now — here’s the part nobody puts on the poster.

The four times you would have quit

That ₹22 crore looks like a miracle today. But living through it was not a miracle. It was an ordeal. If you had been checking your portfolio every quarter, here is what you would have seen — and almost certainly run from:

1. The early years (1994–1998): roughly five years of nothing. For about five years, the value of the investment sat below the money that had been put in. You kept feeding it, month after month, and it kept showing you less than you’d given it. Five years.

2. The dot-com fall (2000–2001): cut by more than half. The portfolio climbed beautifully, then dropped about 56%. More than half — gone. It took roughly three years just to climb back.

3. The 2008 crash: down 66%. This is the famous one. The investment fell from about ₹2.5 crore to ₹86 lakh. Two-thirds of the wealth, vanished on screen. Anyone watching daily would have been sure the game was over.

4. COVID, 2020: down about 31% in a matter of weeks. A sharp, terrifying, vertical drop. The kind that makes your stomach turn.

Four times. Four moments where every instinct in your body screamed “sell, save what’s left, this isn’t working.”

somebody did not act on that scream.

Flat and falling patches are not a malfunction. They are the journey.

I need you to really absorb this, because it is the heart of everything.

When a scheme goes flat for two years, or falls for one year, or trails behind others for a while — that is not a sign that something is broken. That is simply what the road looks like.

There is no equity investment on earth that goes up in a straight line. Not one. The best fund in India still spent years going sideways and months falling like a stone.

So when your portfolio has a quiet year, you have two choices. You can call it “non-performing” and run. Or you can recognise it for what it almost always is: a normal, unavoidable, completely expected stretch of the same long road you signed up for.

“But 32 years? Who has that kind of patience?”

Fair question. Let me answer it honestly, because I don’t want to win the argument with one lucky long example.

So forget 32 years. Let’s take a normal, realistic holding period — the kind a serious investor actually rides. Let’s take the last 15 years, the most recent slice, no cherry-picking. Same fund. Same ₹10,000 a month. Starting July 2011.

In 15 years, that investor put in ₹18 lakh. Today it’s worth about ₹68 lakh — roughly 3.8 times the money, around 16% a year.

And guess what? This “shorter,” “safer” version was also uncomfortable:

- For the first 18 months, the investment was underwater — worth less than what had been put in.

- In 2020, it fell about 30% in weeks.

- In early 2025, it dropped about 15%.

- And right now, as I write this, it is sitting about 5% below its highest point from a few months ago.

So even today — even this lovely 15-year, 3.8x story — looks “not great” if you only glance at the last few months.

That is the trap. Every time frame has a bad-looking window inside it. If you keep zooming into the bad windows, every investment looks like a failure. Including the ones quietly making you rich.

If you want excitement, this is the wrong place

Let me say something gently, but clearly.

If what you want from investing is excitement — a thrill every week, your heart racing up and down with the market, the fun of watching numbers dance — then I have to be honest: mutual funds are not built for that. For excitement, a casino will serve you far better, and far faster.

And one more honest line: if your dream is to see your mutual funds go up in a smooth, straight line, year after year, never falling — please don’t invest in mutual funds. That picture does not exist. Chasing it will only make you miserable, and poorer.

A quick word on comparing the wrong things

Almost every “my fund is not performing” feeling comes from one quiet error: comparing the wrong things.

When someone feels their fund is lagging, they rarely notice that the whole market is down at the same time — that the fund didn’t fail, the season did. And often they’re comparing apples to oranges: an Indian fund against a US one, a steady large-cap against a racy small-cap, a broad multi-cap against one hot sector that’s having its year.

Different things behave differently. Comparing them and feeling cheated is like blaming your scooter for being slower than a motorbike on a day the whole road was jammed anyway.

One car. One driver.

Here is the part I want to say with full humility.

When you come to Moneyplus, we sit down together. We work out your goals, your timelines, how much risk you can actually stomach, what your cashflows look like. Then we choose schemes — after a lot of thought.

But choosing carefully does not mean the schemes will move up in a straight line. They won’t. There will be flat phases. There will be falling phases. There will even be phases where a scheme lags its own benchmark for a while. And in those moments, our job is usually to wait — to give a good scheme three or four quarters to find its feet.

That does not mean we sit blind. We watch every scheme, and we watch every goal. The day a scheme has a real problem — a change of fund manager, a change in its basic character, a genuine reason to worry — we review every single client who holds it, and we act. We’ve even told clients to take their money out as they neared a goal, whether the return was 12% or 15%, simply because the goal was close and the risk no longer made sense.

So the review absolutely happens. We just don’t make noise about it unless there’s a meaningful reason to act. Quiet is not the same as asleep.

But all of this only works if one person is driving.

So let me say this as plainly and as humbly as I can: if you’d rather drive the car yourself — check daily, react quarterly, change funds on a hunch — then please, with complete respect, drive your own car. There is no shame in it. But you cannot have two drivers.

Because I promise you this: nowhere in this world — not at Moneyplus, not anywhere — will you find an investment that climbs 20%, 30% every single year, smoothly, without a single bad patch, for five or ten years straight. That fund does not exist. What exists is a long, bumpy, boring road — and the discipline to stay on it.

So, the only review worth doing

Don’t fire off a message — to me or to anyone — asking “is my fund up this month?” That is the wrong review. It will only ever make you anxious, because the honest answer on any given month is a coin toss.

Ask the question that actually matters instead:

That is the only review worth doing. Notice it has almost nothing to do with what your fund did last quarter — and everything to do with your Why.

Your goal is the signal. Stop staring at the noise.

Let’s talk about your Why — not last quarter’s returns

If you’ve been checking your portfolio every few weeks and feeling that knot in your stomach, that’s not a fund problem — it’s a focus problem. Let’s put it back where it belongs: your goal, your timeline, your cashflow — and whether you’re on track for the life you’re investing toward.

Hitesh Kakkad

This blog is for educational purposes only. The investor described is a composite illustration based on real client patterns — no individual is identified. The fund referenced is used purely as an illustrative example and is not a recommendation. Mutual fund investments are subject to market risk; past performance is not indicative of future returns. Please read all scheme-related documents carefully. ARN-137949.