CAGR vs XIRR — The One Number That Actually Tells You How You’re Doing

Why your portfolio statement shows two return numbers — and which one to actually trust.

Two numbers. One Sunday afternoon.

Meera opens her quarterly statement on a Sunday afternoon.

She has been investing for six years. Started a ₹1,000 SIP in late 2019, stepped it up to ₹2,000 a few years later, and last September even booked a profit — ₹24,944 came back into her bank.

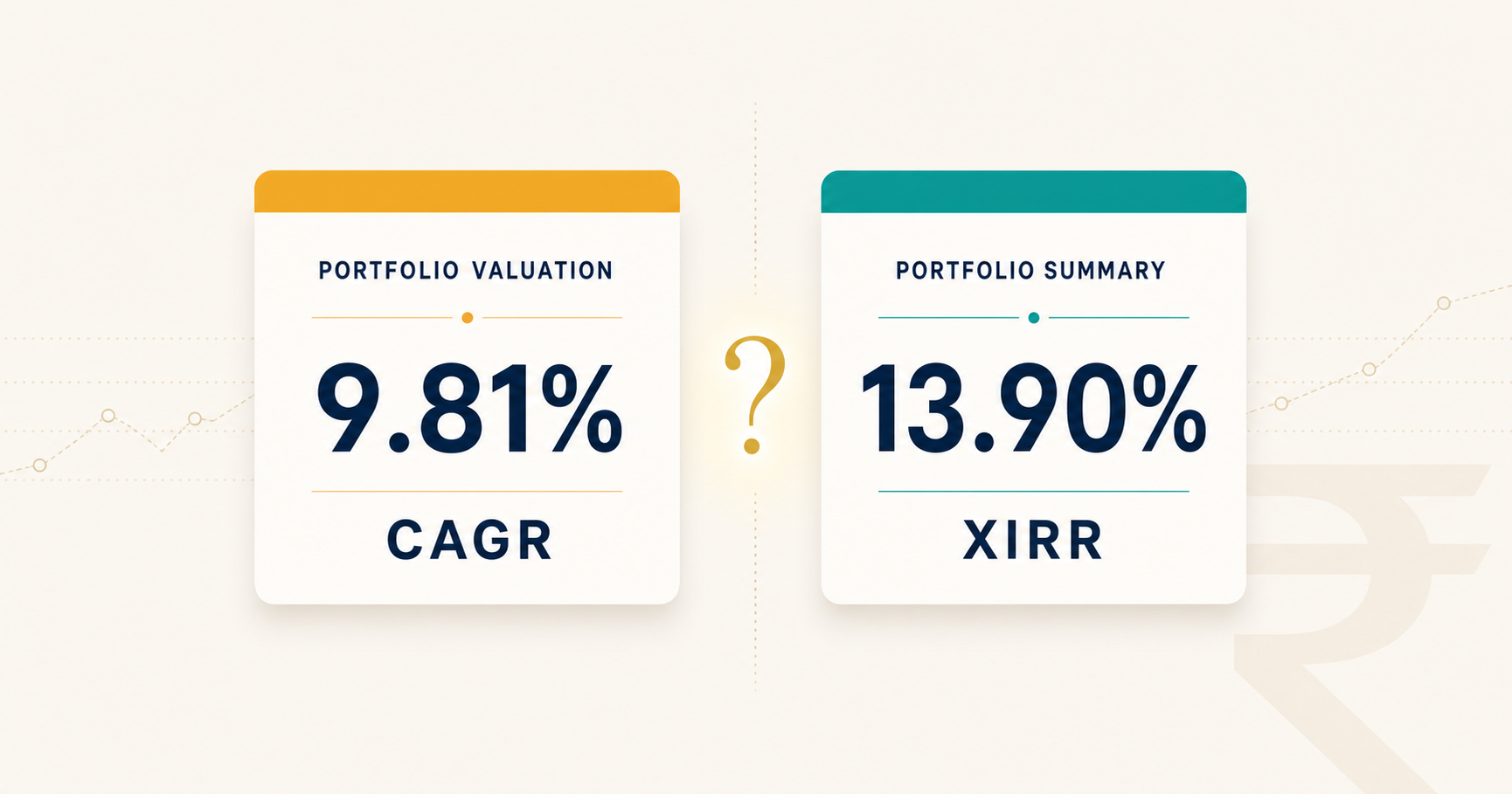

Today, two pages of her statement show her two different numbers.

Page one says her CAGR is 9.81%.

Page two says her XIRR is 13.90%.

Same fund. Same period. Same Meera.

Both are right. They answer different questions.

CAGR asks: “How fast did the asset grow?”

XIRR asks: “How fast did your money grow?”

That distinction sounds small. It is anything but.

The simple case — when CAGR is honest

Arun bought one mutual fund in November 2013 for ₹11,000. He never added to it. He never redeemed from it. He simply forgot about it for twelve years.

Today, that ₹11,000 is worth ₹56,057.

Arun’s statement

CAGR: 13.97% · XIRR: 13.97%

Both numbers identical.

One purchase. One present value. Twelve years in between. CAGR works perfectly here. So does XIRR. They land on the same number because there’s nothing for them to disagree about.

If your investing pattern looks like Arun’s — a single purchase, untouched, given enough time — your CAGR is telling you the truth.

But most of us are not Arun.

Think of it as FD vs RD

A fixed deposit is one transaction. You put money in once. Asking “what was my interest rate?” makes complete sense.

A recurring deposit is different. You add a small amount every month. The first month’s deposit earns interest for the full term. The last month’s deposit earns interest for one month. There is no single “interest rate” — only a more careful average that respects the age of every deposit.

That more careful average is XIRR.

A SIP is the RD.

The moment your investing looks like a recurring deposit, CAGR alone stops being enough.

When CAGR forgets your story — Meera’s journey

Meera’s six years were not just SIPs. She made a small lump-sum top-up during a 2021 market dip. She stepped up her SIP in 2023. And in September 2025 she booked a profit — switched out a portion and put ₹24,944 in her bank.

Meera’s six-year journey

Total invested: ₹1,09,663

Total value today (in fund + already in bank): ₹1,49,761

Statement CAGR: 9.81% · Actual XIRR: 13.90%

A four-percentage-point gap. On a portfolio compounding over decades, that becomes lakhs.

What happened?

she had already taken home.

When you book a profit and the money leaves the fund, the CAGR formula stops counting it. It only looks at “what’s still inside the fund versus what’s still being paid in.” The realised gain — the most satisfying part of your journey, the proof your discipline worked — disappears from the calculation.

XIRR doesn’t forget. Every SIP, every top-up, every switch-out, every step-up — XIRR ties them together with one honest number.

The mirage — when neither number is meaningful

One last case worth knowing.

Suresh invested ₹25 lakh in a multi-asset fund last month. Thirty-seven days ago, to be exact. The fund has gained 3.72% in that short window.

His statement now shows: CAGR 36.68%.

Nothing reliable does.

The platform isn’t lying — it’s just doing the math the formula asks for. CAGR took a 37-day move and projected it into a yearly number. The answer has no real-world meaning yet.

Simple rule

If your investment is less than a year old, ignore the CAGR. Read the absolute return — “my fund is up 3.72%” — and wait.

Twelve months is the minimum honest measurement window for any investment.

Where each number lives in MyMoneyplus

Two reports inside the portal you already use:

- Portfolio Valuation shows CAGR — useful as a quick scheme-by-scheme glance.

- Portfolio Summary shows XIRR — your real return across every transaction.

When you want to know “how am I really doing?” — open the Portfolio Summary.

Access your portfolio anytime

Log in to my.moneyplus.in using your registered mobile number and an OTP. Both reports — Portfolio Valuation and Portfolio Summary — are right there.

What to remember

| Your investing pattern | The number to trust |

|---|---|

| One investment, held for years, never touched | CAGR |

| SIPs, redemptions, switches, step-ups | Only XIRR |

| Less than a year old | The absolute return — ignore the percentage |

That’s it. Three lines.

The Echo

A portfolio is not just the money still sitting inside the fund.

A portfolio is every rupee that went in, every rupee that came back, every step-up that quietly raised the stakes, every profit you booked along the way.

XIRR remembers everything.

When in doubt, look at your XIRR. It knows where you’ve been.

Confused by your portfolio statement?

Five minutes on a call with the Moneyplus team is all it takes to learn how to read your real return correctly.

Very nice example